You don't work in tech. You don't know what a NAV loan is and you don't care. You're a teacher in Ohio, a nurse in Atlanta, a union electrician in Pittsburgh, a firefighter in Phoenix. You've been putting money into your pension every single paycheck for fifteen years and you're counting on it being there when you retire.

Here's what nobody told you.

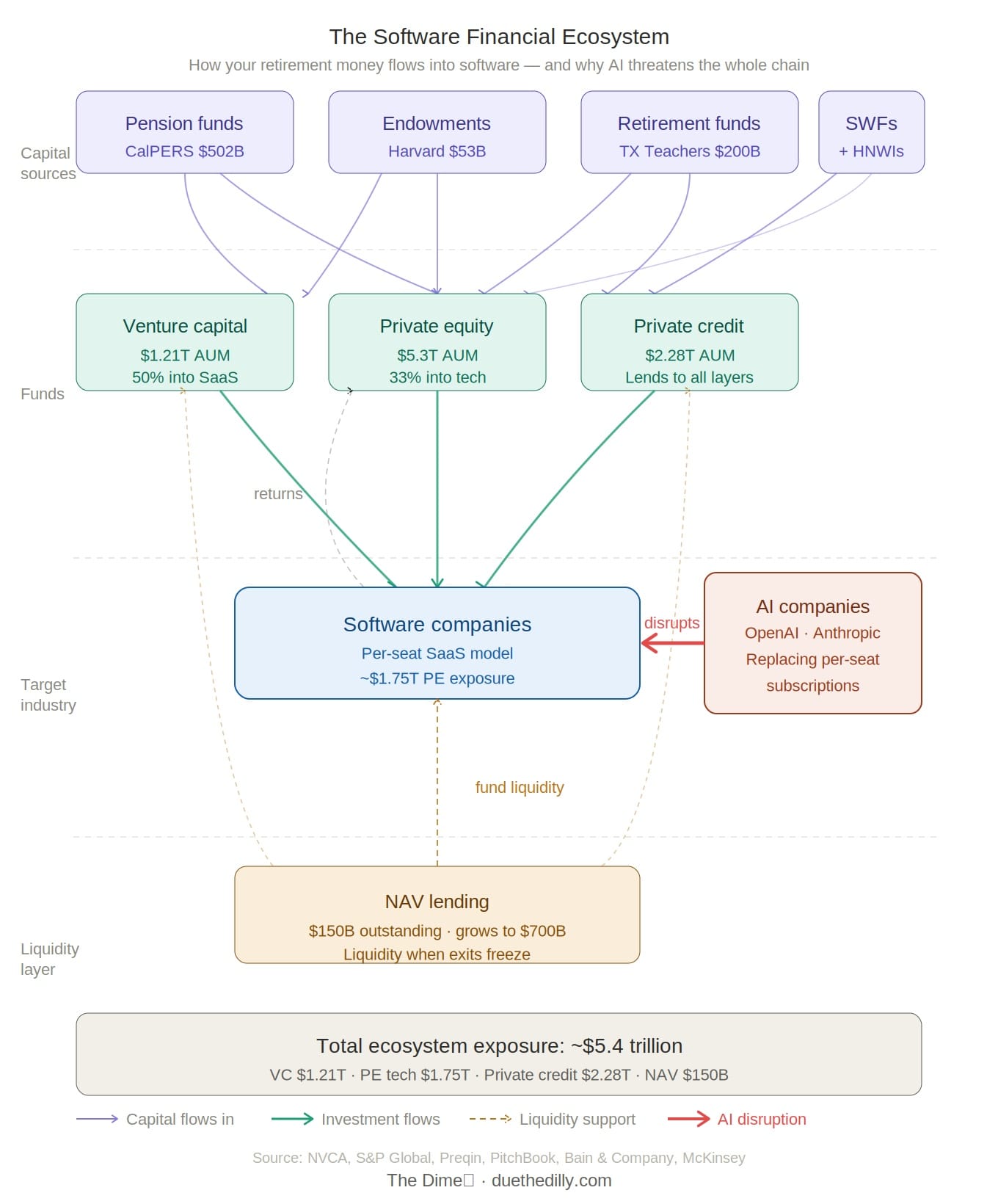

That pension? Your state pension, your union retirement fund, your university endowment if you work in higher education, your 401k if you work in the private sector? It is almost certainly invested in private equity funds, venture capital funds, and private credit funds. And those funds have spent the last decade betting HEAVILY on software companies.

The California Public Employees' Retirement System, CalPERS, the largest public pension in the United States with $502 billion in assets, allocates billions to private equity. The Teacher Retirement System of Texas manages $200 billion and has significant private markets exposure. The New York State Common Retirement Fund, which covers over one million public employees and retirees, manages $267 billion and has been steadily increasing its alternatives allocation. The Harvard University endowment, which funds financial aid and research, manages $53 billion with substantial private equity exposure. None of these institutions invest in software companies directly. They invest in the funds that invest in software companies. The private equity funds. The venture capital funds. The private credit funds.

And right now, the thing those funds bet on most heavily for the last decade is under a structural threat unlike anything those fund managers have ever had to navigate before.

That's why this article is for you, not just for the finance people.

Because if the software financial ecosystem takes a serious hit, the losses don't stay in Silicon Valley. They travel. They travel through the private equity funds, into the pension funds, and eventually into the retirement accounts of people who never wrote a line of code in their lives and never planned to.

You deserve to understand how the dots connect. So let's walk through it.

Let me start with a pattern.

Every major financial correction in modern history has had one thing in common: somebody invented something new, that new thing got wildly overvalued, and then reality showed up and body-slammed it in front of everybody.

The Savings and Loan Crisis of the 1980s? Institutions started making novel loans and investing in financial instruments they didn't fully understand, real estate values collapsed underneath them, and over 1,000 banks failed. The U.S. government had to bail out the wreckage to the tune of $130 billion.

The collapse of Long Term Capital Management in 1998? A hedge fund full of Nobel Prize winners built novel trading strategies using mathematical models so sophisticated that literally nobody outside the firm fully understood them. Then Russia defaulted on its debt, the models blew up, and LTCM lost $4.6 billion in four months. The Federal Reserve had to organize a private sector bailout to prevent a global financial cascade.

The dot com crash of 2000? Venture capital and public markets poured money into internet companies that had no business models, no revenue, and sometimes no actual product, just because the internet was new and exciting and everyone assumed it would change everything. It did change everything, eventually. But first it wiped out $5 trillion in market value in two years.

The Financial Crisis of 2008? Credit default swaps. Subprime mortgages. Mortgage-backed securities. All of it somewhat novel. All of it poorly understood. All of it catastrophically overlevered. And then the housing market turned and the entire system almost went with it.

Notice the pattern? Novel idea. Overvaluation. Reality check. Correction.

But this time feels different. And I mean that in the most unsettling way possible.

This Time the Novel Thing Is Eating the Old Thing

In every correction before this one, new technology or financial innovation disrupted markets. But the underlying industries, the businesses, the assets, the jobs, they mostly survived. The internet had a huge correction but software companies kept growing. The banking industry corrected but lending slowly kept happening.

What we're potentially looking at now is not just a new technology disrupting markets. We're looking at a new technology pushing for the obsolescence of an entire industry category. This is like cars eliminating the need for horses, or electricity eliminating the need for kerosene. But the pace is happening at a faster rate.

We talked about this a last week. Software companies built their entire business model around a per-seat licensing structure. More employees equals more seats equals more revenue. It's a beautiful, predictable, recurring revenue machine. And it's being dismantled seat by seat as AI makes each individual worker more productive, reducing the number of seats companies need to buy.

That's how much private equity is currently betting on software. And public software multiples are down more than one standard deviation from their eight-year average due to the potential of AI disruption.

What we DIDN'T talk about, and what I want to walk y'all through today, is the full economic architecture sitting underneath the software industry. Because this isn't just about software companies losing value. This is about the entire financial ecosystem that was built to fund, grow, buy, and lend against software, and what happens to all of it if the thesis breaks.

So let me lay out every layer of this thing.

Layer One: Venture Capital

This is where it starts. Long before a software company goes public or gets bought by private equity, venture capital finds it, funds it, and builds it.

And between 2020 and 2023, venture capital went ABSOLUTELY nuclear on software.

Global VC funding surged to historic levels in 2020 and 2021. Stimulus policies, digital transformation, and investor optimism pushed funding to $643 to $671 billion in 2021, according to Crunchbase and PitchBook. This period was marked by high valuations, fast deal cycles, and an abundance of capital, particularly in tech-heavy sectors like SaaS, fintech, and digital health.

Y'all. $671 billion in a single year.

Remember all those unicorns? Remember all those companies raising at $1 billion, $5 billion, $10 billion valuations during the pandemic? SaaS has grown to a nearly 50% share of all global venture capital investments. Half. Half of all venture capital money globally went into software subscription businesses.

Then reality showed up. Global venture capital funding dropped to approximately $357 billion in 2022 and further declined to around $214 billion in 2023, reflecting a more cautious investment environment. This represents a 40% year-over-year decrease from 2022 to 2023.

So the VC industry bet hundreds of billions on software during the boom years. Many of those bets haven't been resolved yet. The companies are still private, still holding those inflated valuations on paper, and the exit market has been largely frozen. Holding periods are the longest they've been in a decade. That means the money is locked up, and the question of what it's actually worth is about to get answered. In a market where AI is eating the business model those companies were built on.

Total US VC assets under management: $1.21 trillion as of 2023, according to the NVCA.

Layer Two: Private Equity

After VC, private equity steps in. They buy the mature software companies, optimize them, load them with debt, and flip them to a bigger buyer or the public markets.

Private equity remains the largest private market asset class with global AUM of $5.3 trillion as of 2023.

And software has been PE's favorite toy for over a decade. The technology sector remained private equity's staple, representing 33% of buyout deals by value and 26% by volume. So if you take 33% of $5.3 trillion in global PE AUM, you're looking at roughly $1.75 trillion in private equity exposure to technology, the majority of which is software.

Let me put that plainly. Private equity is sitting on over 16,000 companies it has held for more than four years and hasn't been able to sell yet. Many of them are software companies. The exit market is backed up. And the very thing that was supposed to make these companies valuable, their per-seat subscription revenue and predictable ARR growth, is now the thing under AI threat.

We already talked about what happened to Thoma Bravo and Medallia. That $5.1 billion write-off is the loudest example. It will not be the last.

Layer Three: Private Credit

Now here's the layer most people don't think about. Because it's not just equity money in these companies. There's a massive amount of DEBT.

As of 2025, global private credit assets under management have surpassed $2 trillion, a staggering tenfold increase since 2009.

But here's the part that really matters for this article. Private credit isn't just lending to software companies directly. They're lending to the private equity firms that own the software companies. When ThomaBravo buys a software company, they put equity in, but they also put debt in. That debt comes from private credit. So when the software company struggles, it's not just the equity that's at risk. The private credit lenders are sitting there too, in the capital structure, waiting to get paid.

The AUM of private credit assets is expected to nearly double to $4.504 trillion in 2030 from an estimated $2.280 trillion in 2025, according to a report by Preqin.

And on top of lending to software companies and PE firms, private credit is also financing the AI data centers being built by the technology companies doing the disrupting. So the same pool of private credit capital is simultaneously funding the companies being disrupted AND the companies doing the disrupting. That is a genuinely wild situation.

Private credit total: $2.28 trillion and growing.

Layer Four: NAV Lending

And then on top of ALL of that, we have NAV lending.

When private equity and venture capital funds need liquidity for their investors but can't exit their positions because the market is frozen, they borrow against the value of what they own. That's a NAV loan. It's how the whole machine keeps moving when exits are slow.

So right now there's $150 billion in NAV loans outstanding, secured against the portfolios of PE and VC funds. Many of those portfolios have significant software exposure. If software valuations continue to get crushed by AI disruption, the NAV calculations get challenged, the loan covenants get stressed, and the lenders start making phone calls.

NAV lending total: $150 billion outstanding, projected to reach $300 billion within two years and $700 billion total addressable market by 2030.

So What's the Total Economic Value at Stake?

Let me add this up for y'all. And I'm being conservative because some of these categories overlap.

| Layer | Estimated Exposure |

|---|---|

| Venture Capital AUM | $1.21 trillion |

| Private Equity (tech/software share) | ~$1.75 trillion |

| Private Credit AUM | $2.28 trillion |

| NAV Lending Outstanding | $150 billion |

| Total | ~$5.39 trillion |

Five. Point. Four. Trillion. Dollars.

To put that in perspective? The entire U.S. subprime mortgage market at the peak of the 2008 financial crisis was approximately $1.3 trillion. The total losses from the 2008 crisis were estimated at around $2 trillion globally. What we're looking at here, in terms of total capital at risk across the software financial ecosystem, is potentially MORE than two times the total losses of the worst financial crisis since the Great Depression.

Now, is ALL of this going to zero? No. Not every software company is going to be disrupted. Not every PE deal is going to blow up. Not every private credit loan is going to default. But the concentration of risk, the interconnected nature of it, and the structural nature of the threat, which isn't a recession or a rate shock but a TECHNOLOGY DISPLACEMENT, makes this unlike anything the financial world has navigated before.

Every previous correction had a solution. Lower rates. Government bailout. Wait for the cycle to turn. The dot com companies eventually recovered, because the internet was still real and still valuable.

But if your software company's revenue model is being made structurally obsolete by AI, you can't just wait for the cycle to turn. The cycle isn't turning back.

And The Jobs. Let's Talk About The Jobs.

Behind all these trillions of dollars are real people with real jobs.

6 million tech workers. Median salary over $100,000. The median annual wage for this group was $105,990 in May 2024, which was higher than the median annual wage for all occupations of $49,500.

These are middle class, upper middle class, and frankly in many cases wealthy jobs. They are the jobs that pay mortgages in San Francisco, Austin, New York, Seattle, and Raleigh. They are the jobs that fund 401ks, pay property taxes, support local economies, and buy the goods and services that keep other people employed.

The tech sector employs 6 million people directly. Every tech job supports an estimated 4 to 5 additional jobs in the broader economy through spending and supply chain effects. So the total employment impact of this sector, when fully counted, is somewhere between 25 and 30 million American jobs.

If a significant portion of software companies lose revenue to AI displacement, and the private equity firms that own them can't service their debt, and the private credit firms that lent to everyone start seeing defaults, and the NAV loans supporting the whole liquidity structure get stressed, the job losses don't stay in Silicon Valley.

They spread.

Don't be stingy with the 🏀. Pass it to a friend.

See y'all next week.

CJB

This is not legal advice, financial advice, or attorney advertising. This newsletter is for educational and informational purposes only. For actual guidance on investments or financial decisions, please consult a licensed financial advisor. The numbers cited throughout this article are sourced from NVCA, S&P Global, Preqin, PitchBook, Bain & Company, McKinsey, the U.S. Bureau of Labor Statistics, and CompTIA. Don't be out here making moves based on a newsletter. You're smarter than that.